2. Disrupted global supply chains

For years, the cornerstones of supply chain management have been globalisation, low-cost supplies and minimal inventories.

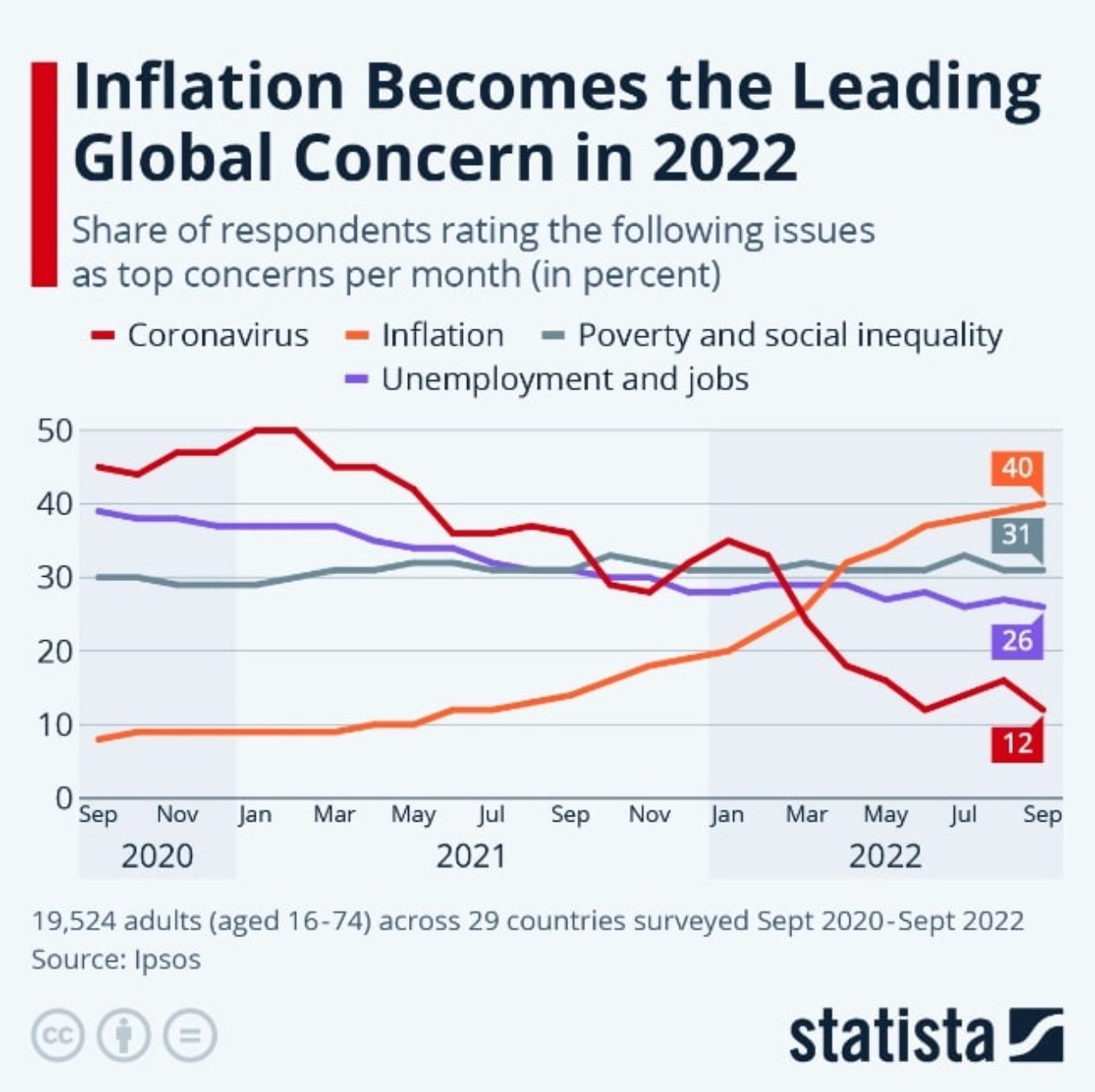

However, COVID-19 broke supply chains around the world and its impact cannot be understated. It forced companies to build supply chain resilience and assess how future interruptions can be avoided and systems reestablished quickly if need be.

Unfortunately, supply chain disruptions are becoming ever more frequent and harsh. According to McKinsey, disruptions to manufacturing production occur now about every 3.7 years.

Experts predict that systems could “normalise” in 2023. But even if they do, the pandemic exposed global logistic network vulnerabilities to future political instability, natural disasters, and regulatory changes.

Supply-chain resilience has, therefore, emerged as business-critical.

3. M-commerce will continue to expand

One of the forces driving the growth of online retail commerce is the global use of smartphones and tablets.

Both retailers and shoppers are increasingly using mobile shopping apps, with one in five US shoppers reporting using them multiple times per day. Branded shopping apps, 5G wireless and social shopping have all converged to make this mobile commerce – or m–commerce – smoother.

In fact, mobile-commerce was predicted to take up 6 percent of total retail sales in 2022, a rise from 4.1 percent in 2019. And by 2025, social commerce sales – those taking place on platforms such as Facebook, Instagram and TikTok – are estimated to triple.

Nearly half of China’s consumers already shop on social and we can expect to see further growth across all markets with the rise of branded shopping apps, more SMS and Facebook Messenger marketing campaigns and greater social commerce content on TikTok and Instagram.

4. The emergence of live shopping and mixed channels

An extension of these m-commerce channels is also emerging in the increasingly popular live shopping.

For the uninitiated, this phenomenon is based on the belief that the future of shopping is video. It provides an experience most closely resembling in-person shopping where buyers can watch people (eg. influencers) try on products in real time and comment. Think television shopping channels shopping of the 1970-80s that specialised in selling home goods, fashion and beauty products. The concept is the same but now takes place on mobile phones.

Live shopping has completely taken off in China where the live market is forecasted to increase from $2.27 billion in 2021 to $4.92 billion in 2023. It’s emerging as a marketing channel in other markets also, such as the US, where 20 percent of online shoppers said they’d participated in live commerce.

According to McKinsey, live commerce sales could account for as much as 20 percent of all e-commerce by 2026.

5. The dominance of China and APAC

According to projections, retail e-commerce sales in Asia-Pacific will be greater than the rest of the world combined by 2023.

In 2022, for example, China’s e-commerce sales totalled approximately $2.8 trillion. That’s more than double the US market. And this disparity is even more pronounced in B2B, as APAC and China continue to improve their industrial structures.

It must be remembered that with around 632 million internet users, China is the fastest-growing and largest e-commerce market in the world.

Takeaway

All the data, market research and trends speak of an e-commerce market that has become and will continue to be a significant part of the global economy. Despite facing some headwinds, the market will continue to grow, providing e-commerce fulfilment facilities plenty of opportunities for increased growth. In servicing this market, however, it will be important that fulfilment centres work to optimise their operations to reduce costs and resources through increased use of automation and digital technologies.